Original Link: https://www.anandtech.com/show/7112/the-arm-diaries-part-1-how-arms-business-model-works

The ARM Diaries, Part 1: How ARM’s Business Model Works

by Anand Lal Shimpi on June 28, 2013 12:06 AM EST

It must frustrate ARM just how much attention is given to Intel in the ultra mobile space, especially considering the chip giant’s effectively non-existent market share. Since 2008 Intel has tried, year after year, to break into smartphones and tablets with very limited success. Despite having the IP and technical know-how to do so, it wasn’t until 2012 that we saw Intel act like a company with even a sliver of a chance. Today, things are finally starting to change. Intel’s 22nm SoC process and updated Atom microarchitecture look very competitive, and we’ll see the first tablet products based on them later this year - with phones following sometime in early 2014. As Intel is about to start acting like a competitor, ARM is starting to talk a lot more about its magic.

We’ve had well over a decade of Intel sharing its beliefs with us, but this is ARM’s first attempt at doing the same. What will follow over the next few posts are a bunch of disclosures, some related some not, attempting to bring everyone up to speed on where ARM is today and where ARM will be in the near future. The best place to start is with ARM’s business model.

In the PC industry, the concept of a fabless semiconductor manufacturer isn’t unusual. NVIDIA has always been one, and now AMD is one as well. Fabless semiconductors create all of the designs for their chips, but they’re physically manufactured at a foundry partner (e.g. TSMC, Global Foundries, Samsung). The fabless semi approach greatly helps reduce costs, but your designs are ultimately at the mercy of your foundry partner. Capacity, quality of process and timeline for process are more or less out of your control. Sometimes this is a non-issue, but other times it dramatically impacts your ability to bring products to market (e.g. quality control for early TSMC 40nm, timeline for GF 28nm or early capacity for TSMC 28nm).

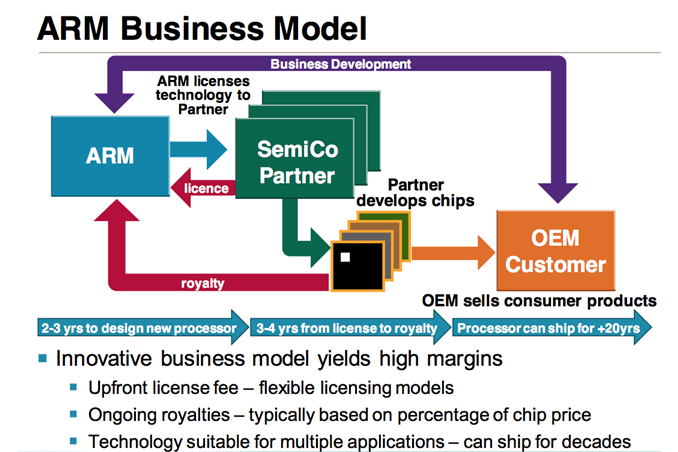

ARM goes one step beyond the fabless semi: it doesn’t even sell any chips into the marketplace. ARM instead, designs IP (instruction set architecture, microprocessor, graphics, interconnects) and licenses it to anyone who wants to use it. ARM’s customers will then take the IP they’ve licensed and design it into silicon. These customers can be fabless semiconductor companies or companies that own fabs.

It’s a very unique business model, especially if you compare it to that of the market share leader in the PC silicon space (Intel). From Intel’s perspective, it made the mistake of licensing the x86 ISA early on in its life, but quickly retreated from that business. It instead builds its own architectures, designs them into chips for various markets, and manufactures the designs at its own foundries. Intel is a truly vertically integrated chip design and fabrication house. It’s a lot of work, but Intel is rewarded by having extremely high margins on all of its products.

The ultra mobile world is very different, at least today. In the PC world, Intel drives platform definition and ends up being the biggest part of the BoM (Bill of Materials) as a result. In smartphones and tablets, the main applications processor is easily under 10% of the cost of the device. More often than not, we’re talking about low single digit percentages of the total BoM (e.g. $15 SoC for a $400 device, or 3.75%). Intel’s theory is that this will eventually change as silicon complexity increases inside ultra mobile devices, but until now (and likely for the near future) the market requires/enables a different sort of business model.

How ARM Works

The ARM business model is incredibly simple to understand, it’s just different than what we’re used to in the PC space. At a high level, ARM offers three different types of licenses: POP, processor and architecture.

A processor license is the license to use a microprocessor or GPU that ARM has designed. You can’t really change the design, but you get to implement it however you’d like. For example, Samsung’s Exynos 5 Octa implements four ARM Cortex A7 cores and four ARM Cortex A15 cores - these are processor licenses. ARM will provide guidelines as to how to implement these designs in silicon, but ultimately it’s up to you and your physical implementation teams to do so and get good frequency/power out of your design.

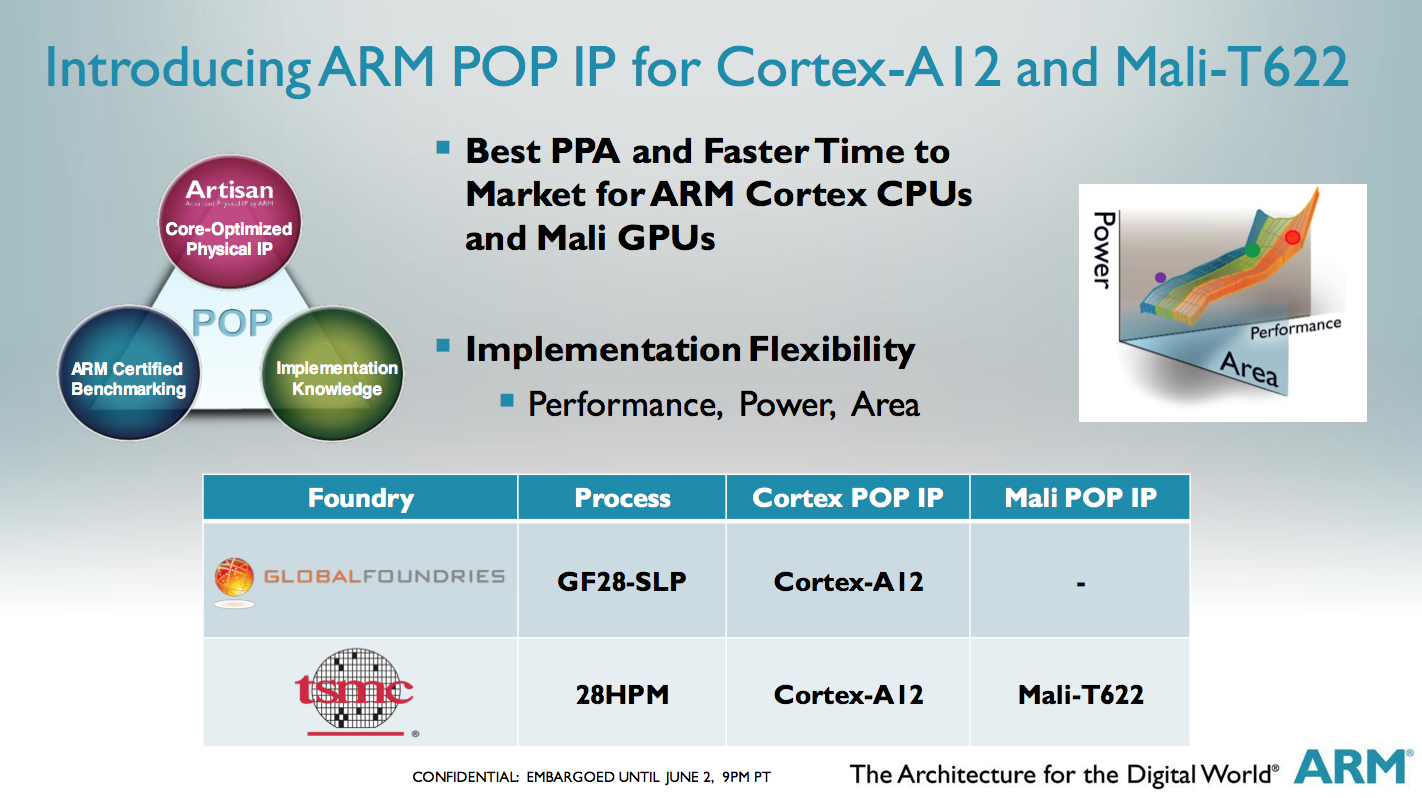

A processor optimization pack (POP), takes a processor license to the next level. If you aren’t great at physical implementations, ARM will sell you an optimized processor design that you can take and manufacture at a specific foundry which will result in some degree of guaranteed performance. If you look at what happened with the Cortex A8, Apple and Samsung had their own physical implementations of the core that resulted in better frequency/power than a lot of other designs. Apple and Samsung had access to Intrinsity who hardened the Cortex A8 design, but not all companies had the bandwidth/budget to do the same. POPs are ARM’s equivalent solution for those customers who need very good implementations but can’t do so by themselves. POPs are available for various processor/foundry/process node combinations. For example, ARM offers a 28nm HPM POP at TSMC for the Cortex A12.

The final option is an architecture license. Here, ARM would license you one of its architectures (e.g. ARMv7, ARMv8) and you’re free to take that architecture and implement it however you’d like. This is what Qualcomm does to build Krait, and what Apple did to build Swift. These microprocessors are ISA compatible with ARM’s Cortex A15 for example, but they are their own implementations of the ARM ISA. Here you basically get a book and a bunch of tests to verify compliance with the ARM ISA you’re implementing. ARM will offer some support to help you with your design, but it’s ultimately up to you to design, implement and validate your own microprocessor design.

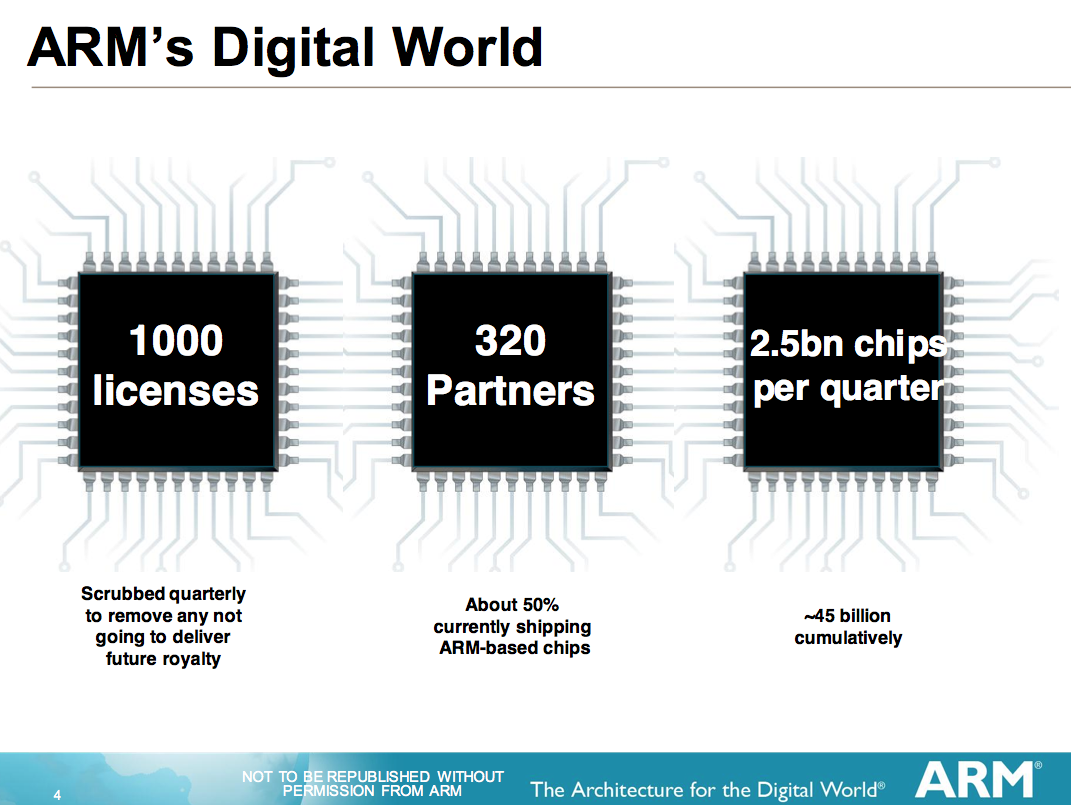

In terms of numbers, ARM has around 1000 licenses in the market spread across 320 licensees/partners. Of those 320 licensees, only 15 of them have architecture licenses.

How ARM Makes Money

AMD, Intel and NVIDIA all make money by ultimately selling someone a chip. ARM’s revenue comes entirely from IP licensing. It’s up to ARM’s licensees/partners/customers to actually build and sell the chip. ARM’s revenue structure is understandably very different than what we’re used to.

There are two amounts that all ARM licensees have to pay: an upfront license fee, and a royalty. There are a bunch of other adders with things like support, but for the purposes of our discussions we’ll focus on these big two.

Everyone pays an upfront license fee and everyone pays a royalty. The amount of these two is what varies depending on the type of license.

The upfront license fee depends on the complexity of the design you’re licensing. An older ARM11 will have a lower up front fee than a Cortex A57. The upfront fee generally ranges from $1M - $10M, although there are options lower or higher than that (I’ll get to that shortly).

The royalty is on a per chip basis. Every chip that contains ARM IP has a royalty associated with it. The royalty is typically 1 - 2% of the selling price of the chip. For chips that are sold externally that’s an easy figure to calculate, but if a company is building and selling a chip internally the royalty is based on what the market price would be for that chip.

Both the up front license fee and the royalty are negotiable. There are discounts for multiple ARM cores used in a single design. This is where things like support contracts come into play.

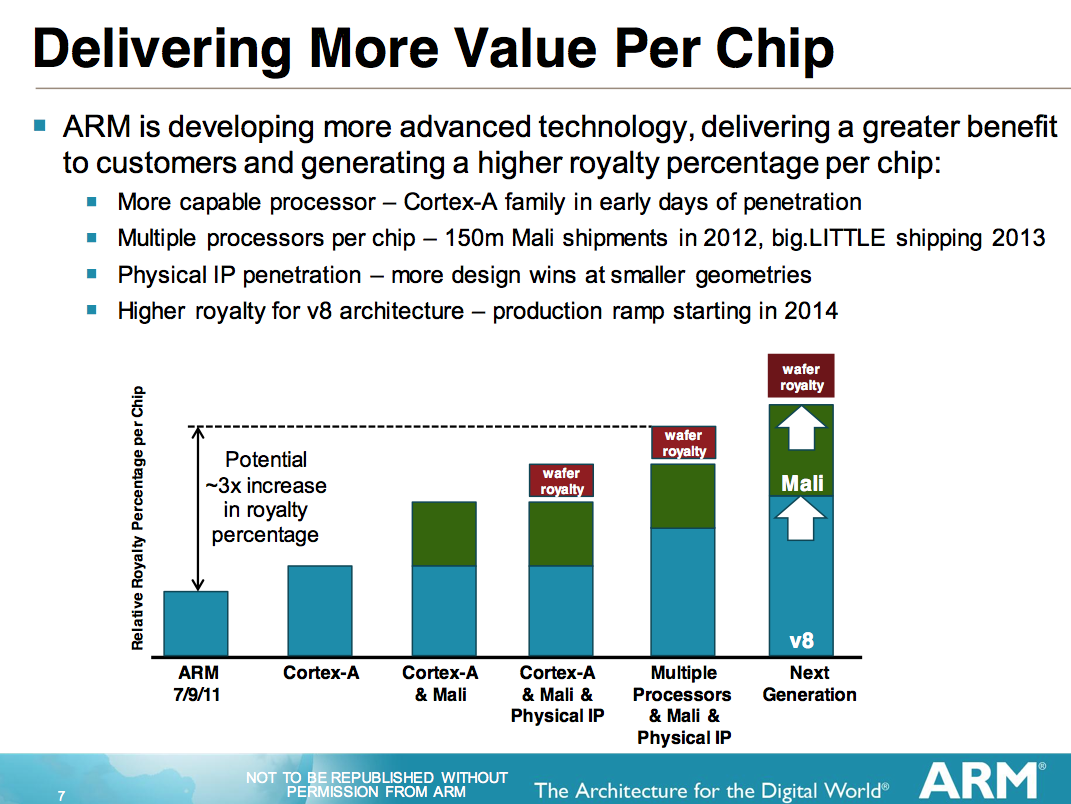

Buses/interfaces come for free, you really just pay for CPU/GPU licenses. ARM’s Mali GPU is typically going to be viewed as an adder and is currently viewed as demanding less of a royalty than ARM’s high-end CPU licenses. A rough breakdown is below:

| ARM Example Royalties | ||

| IP | Royalty (% of chip cost) | |

| ARM7/9/11 | 1.0% - 1.5% | |

| ARM Cortex A-series | 1.5% - 2.0% | |

| ARMv8 Based Cortex A-series | 2.0% and above | |

| Mali GPU | 0.75% - 1.25% adder | |

| Physical IP Package (POP) | 0.5% adder | |

In cases of a POP license, the royalty is actually paid by the foundry and not the customer. The royalty is calculated per wafer and it works out to roughly a 0.5% adder per chip sold.

It usually takes around 6 months to negotiate a contract with an ARM licensee. From license acquisition to first revenue shipments can often take around 3 - 4 years. Designs can then ship for up to 20 years depending on the market segment.

Of the 320 companies that license IP from ARM, over half are currently paying a royalty - the rest are currently in period between signing a license and shipping a product. ARM signs roughly 30 - 40 new licensees per year.

About 80% of the companies that sign a license end up building a chip that they can sell in the market. The remaining 20% either get acquired or fail for other reasons. Royalties make up roughly 50% of ARM’s total revenues, licensing fees are just over 33% and the remainder is equally distributed between software tools and technical support.

ARM's revenues are decent (and growing), but it's still a relatively small company. In 2012 ARM brought in $913.1M. Given how many ARM designs exist in the market (and the size of some of ARM's biggest customers), it almost seems like ARM should be raising its royalty rates a bit. Because of ARM's unique business model, gross margin can be north of 94%. Operating margin tends to be around 45% though.

Types of License

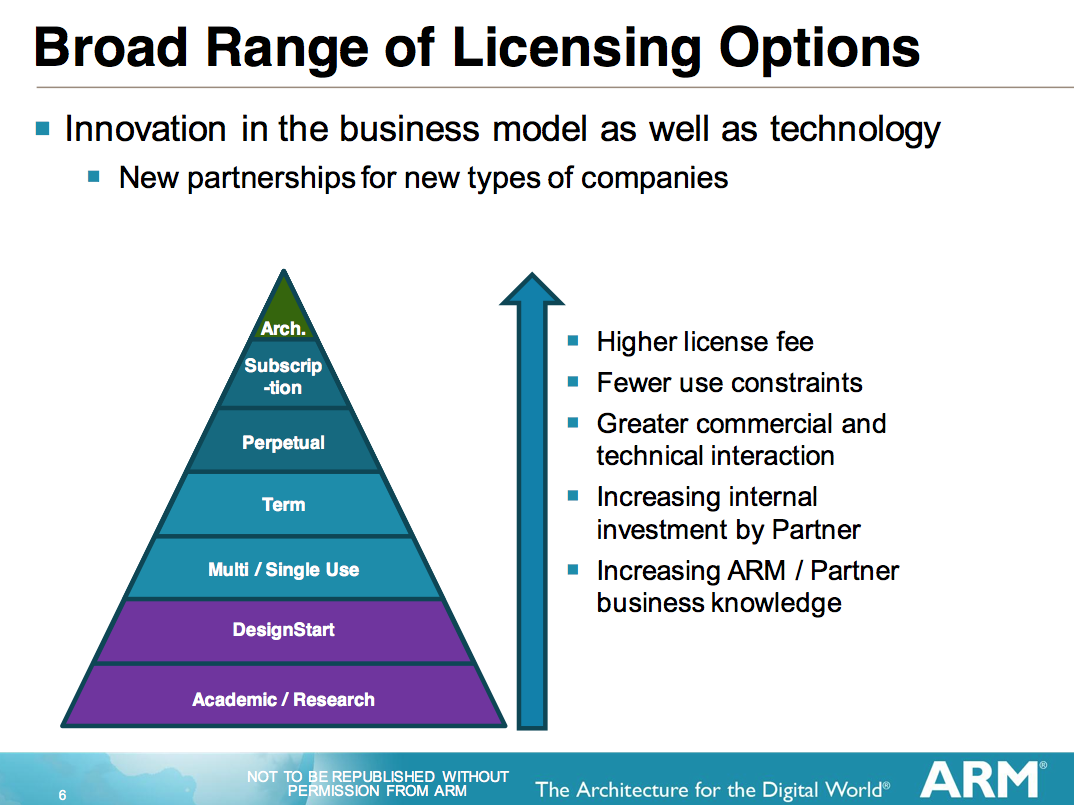

Although I wrote about there being three high level license types (processor, POP and architectural) in reality there’s a spectrum of options that ARM offers.

Academic licenses are effectively free. You can’t sell any designs but it’s a great way to build familiarity with an architecture. DesignStart is a low cost option for an academic/research arm of a company. Again, neither of these designs can be sold which is why the up front fee is very low/effectively zero.

ARM offers single use licenses for companies who just need a particular core for a single project (e.g. I want to build a single design based on the Cortex A9). A single use license for a Cortex A-class CPU will be somewhere around $1M up front plus ~2% per chip sold. The single use licenses are really useful for startups or very specific design needs within a company.

Multi-use licenses make a bit more sense for larger companies with multiple products. Here you get a larger up front fee but you can use your licensed CPU design within any number of products within a certain period of time (e.g. 3 years). During that time frame you can design as many products as possible, but you cannot begin any new designs after the 3 year period ends without a license renewal.

Perpetual multi-use licenses are more common in larger companies. These allow the licensee to use a core in any number of devices, indefinitely. As some ARM licensees can keep the same core in use for 10 - 20 years (particularly in industrial applications), the perpetual multi-use license gets a fair bit of use.

The subscription license is quite possibly the most interesting out of the pyramid. Companies can purchase a subscription license to ARM’s entire portfolio of products, for a set number of years. What a subscription license really enables is engineering managers within a company to start a chip project without having to worry about asking for budget for a large up front license fee since the company as a whole has already paid it. The up front fee here is multiple times the $10M top end for a standard part, for obvious reasons.

Finally at the top of the pyramid is an ARM architecture license. Marvell, Apple and Qualcomm are some examples of the 15 companies that have this license.

The Chosen Three

Since ARM doesn’t actually make any chips of its own, it needs to ensure that for each generation there are launch partners that will produce designs based on the latest and greatest. For each new microprocessor IP, ARM chooses up to three partners to work very closely with. The reason for choosing three is to hopefully work with companies targeting multiple markets. We tend to focus on the high-end smartphone/tablet SoC space here, but ARM architectures find their way into industrial, digital home, TV and other markets as well.

These companies get earlier access than any other licensee to whatever new microarchitecture ARM is working on. The licensees in exchange help debug and test the IP, even providing feedback directly to ARM. The benefit to the licensee is the potential for a significant time to market advantage on the new microarchitecture.

Market Share

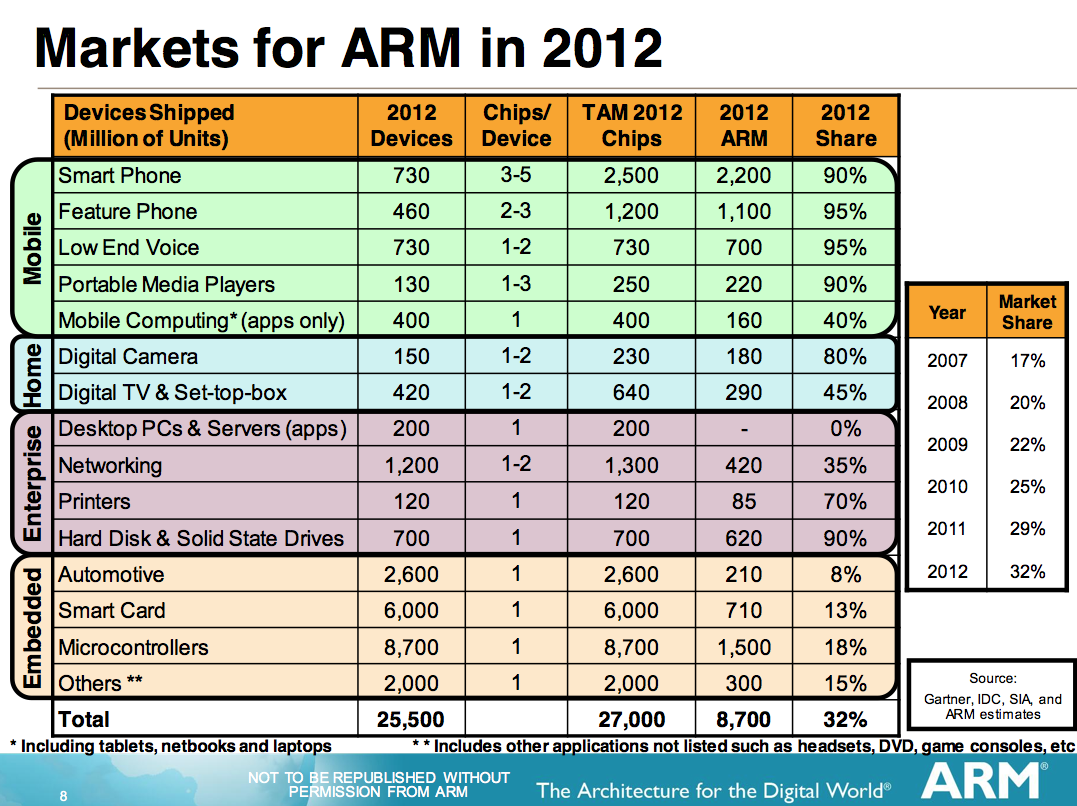

In 2012, ARM licensees shipped around 8.7 billion chips. Depending on the market segment, a single device can have anywhere from one to many ARM cores in it. Even looking within a smartphone you have multiple ARM cores not only within the apps processor but also inside the modem.

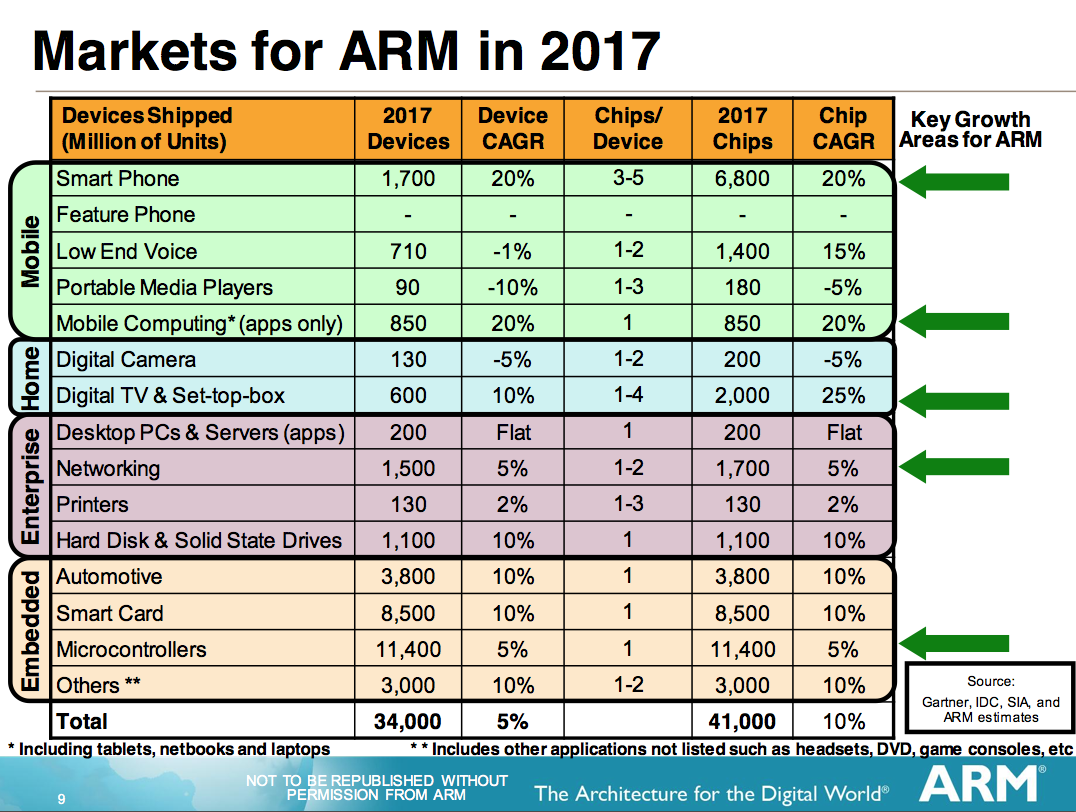

Although ARM has tremendous market share within the ultra mobile space (90%+), more than half of its shipments come from other segments. Enterprise, digital home, TVs, etc... are all expected to be drivers of growth for ARM in the coming years. By 2017 ARM expects its customers to be shipping roughly 41 billion chips that use ARM IP every year.

Final Words

Business models that leverage the scale and strength of a distributed production model are often very disruptive. ARM designs IP that can be implemented by fabless and fully integrated semiconductor companies very quickly, and at relatively low cost. No one member of the supply chain has to assume a significant amount of risk relative to others in the chain. It’s a far more democratic and partner centric approach to chip supply, which is one reason that it’s done so well.

ARM’s business allows for the creation and sustainability of several chip companies, which in turn keeps prices very low and prevents consolidation of power in any one firm. Although other factors (e.g. modem business, patent licensing) have lead to dominance in specific markets, ARM’s overall impact on the industry is one of promoting competition and keeping (silicon) prices low. ARM quite obviously enables what Qualcomm calls the Internet of things, where nearly everything is connected and computes.

It’s important to note that although our focus on ARM tends to be in the smartphone and tablet space, the majority of its licensed shipments come from other areas. It’s quite likely that ARM’s chances for future growth in terms of margin are in higher-end mobile SoCs, but competition from Intel in one segment surely won’t be the end of the world for ARM.

In the coming parts I’ll be taking a look at some of ARM’s newly announced microprocessor architectures such as the Cortex A12, A53 and A57. I’ll also be looking a little deeper into big.LITTLE and Mali graphics.